Traditional Mortgages Are Holding You Back

—Here’s What Smart Investors Are Doing Instead

—Here’s What Smart Investors Are

Doing Instead

Banks use outdated rules that limit your borrowing power and slow down your growth. But with the right strategy, you can skip the roadblocks and scale your portfolio faster.

Traditional mortgages are NOT built for real estate investors

Banks limit how much you can borrow based on your personal income, making it nearly impossible to scale.

The result?

You hit a borrowing cap and can’t buy more properties

You waste time on paperwork, W2s, and tax returns

You miss out on deals because banks take too long to approve you

It’s NOT your fault. The system is built for 9-to-5 workers—not investors

The system is broken. But smart investors have found a better way

The secret? Stop using your personal income to qualify

Here’s the truth: You don’t need to prove your personal income.

You just need a property that cash flows or simple bank statements

Debt-Service Coverage Ratio (DSCR) Loans let you use rental income to get approved

—not your job income.

If the property cash flows,

you qualify.

No W2s. No tax returns. No personal income verification.

Buy in your LLC’s name and protect your assets

This is how top investors scale faster

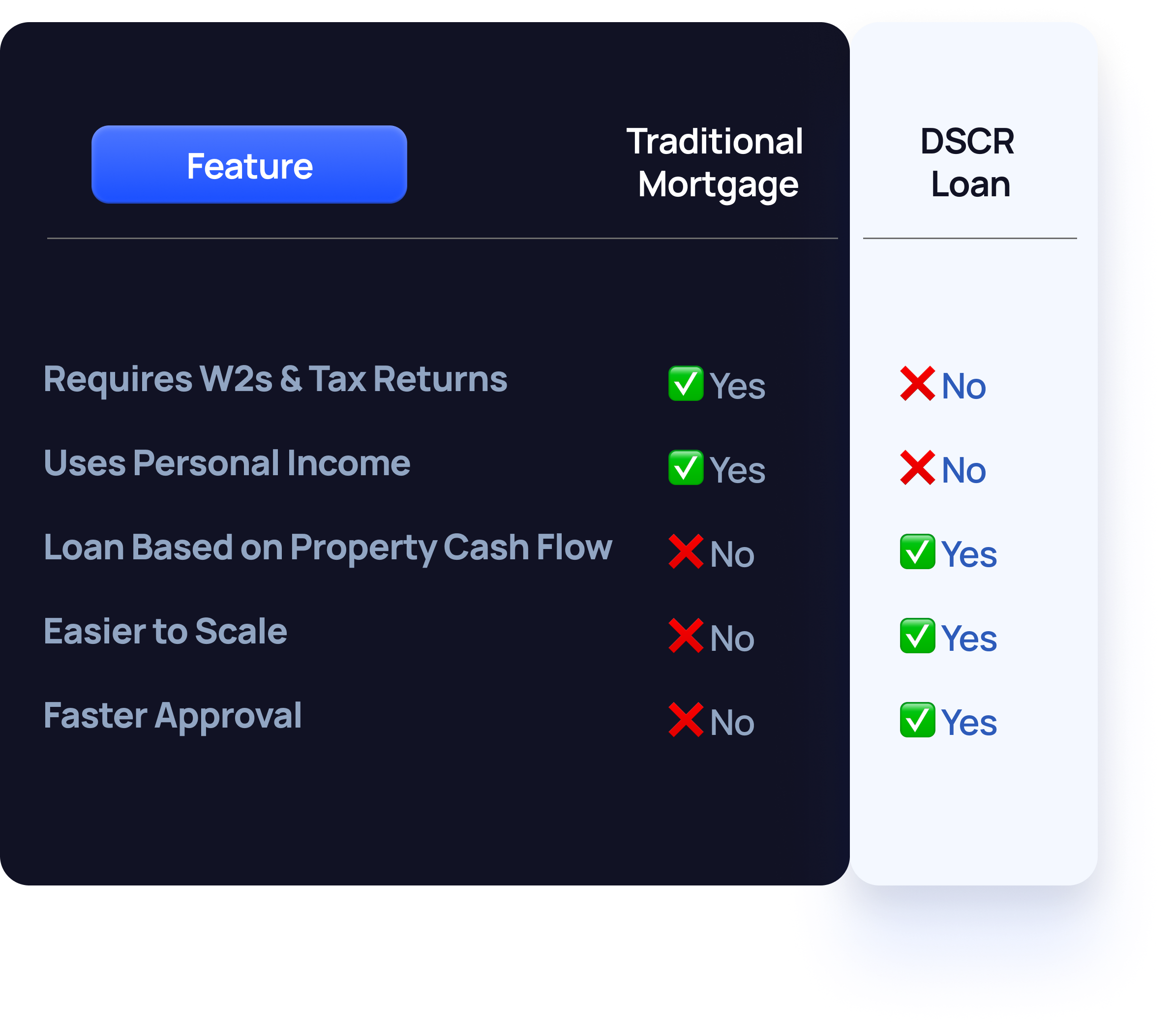

Traditional Mortgages vs. DSCR Loans

Follow Me on Instagram for More Real Estate Financing Hacks!

Follow Me on Instagram for More Real Estate Financing Hacks!

Committed to giving you all the support and guidance you need to find the right mortgage options for you and your family.

Frequently Asked Questions

Can I use a DSCR loan if I’m a first-time investor?

Yes! Many first-time investors use DSCR loans to buy their first property.

Do I need a high credit score?

No! You can qualify with a 620+ credit score

Aren’t DSCR loan rates higher?

Slightly, but you gain WAY more flexibility and can scale faster.